In recent years, Buy-Now-Pay-Later (BNPL) companies like Afterpay, Zip, and Humm have taken over the Australian industry, transforming the look of online payments. BNPL platforms accept BNPL payments, allowing consumers to complete transactions and pay the balance in instalments with no interest. According to BNPL statistics of 2023, BNPL Australians spent more than $22.9 billion in GDP, and BNPL also supported almost 150,000 jobs in Australia. Surveys show that over 59% of Gen Z and Y consider BNPL schemes for e-commerce payments better than other options. Nonetheless, the expansion of BNPL has elicited debates on the likelihood of higher debt levels for households and credit risk. The Reserve Bank, the Australian government, and BNPL firms will add more BNPL regulations , such as late payment fees and credit checks for consumers. However, BNPL usage remains high due to the dynamic development of digital payment solutions and the widespread use of BNPL payment as a preferred option compared to credit resources, which offer a viable and attractive solution to online purchasing capabilities. Let's learn more about BNPL services in this article!

Growth of Buy Now, Pay Later (BNPL) Services in Australia

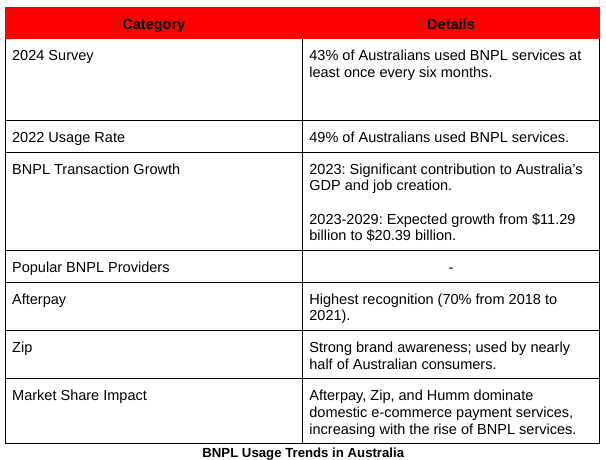

BNPL usage has indeed taken Australia by storm, and this has especially happened in the past few years. According to a survey conducted in July 2024, 43% of Aussies had employed BNPL services to purchase commodities at least once every six months; nonetheless, BNPL use has progressively increased over the years, with the outstanding rates being 49% in 2022.

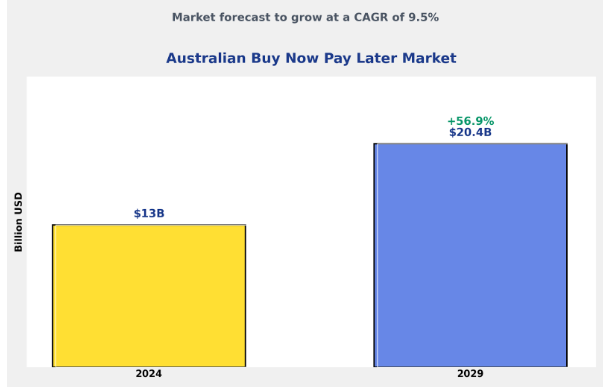

Transaction volumes for BNPL have also increased remarkably. In 2023, the BNPL industry greatly influenced Australia’s GDP and helped create employment opportunities. The value of BNPL transactions in Australia is expected to reach $11.29 billion from 2023 to $20.39 billion by 2029 . This growth is because the BNPL is becoming more popular among consumers as an option when shopping online.

The country owns the largest market share of BNPLs, which mainly include Afterpay, Zip, and Humm. Afterpay has the highest recognition among consumers, with 70% from 2018 to 2021. Zip is the second option with strong brand awareness; almost half of Australian consumers use it. These players have secured a large market share for domestic e-commerce payment services, which has increased with BNPL services.

Demographic Breakdown of BNPL Users

There has been an increase in the use of buy now, pay later services, which enable consumers to purchase goods and services through delayed payment options on the Internet. The latest figures indicate that the uptake of BNPL remains high across various consumer segments.

Age Distribution

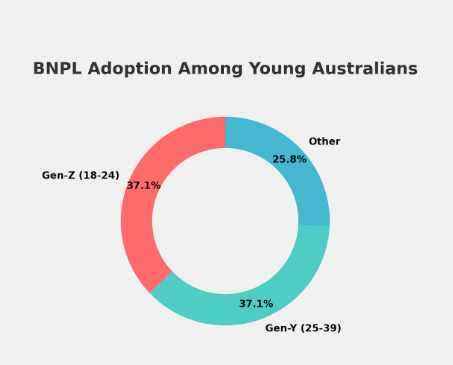

Survey participants indicated that young people in Australia rely most on BNPL services to shop online. The report shows that 59% of the Gen-Z population between the ages of 18 and 24 and 59% of the Gen-Y population ages 25 to 39 find BNPL most appealing. Younger adoption rates also demonstrate that they are interested in other, more adaptable forms of payment than credit cards.

Gender Distribution

While everyone can use BNPL services, a Market report analyzing the BNPL sector in 2023 found that male users were slightly higher than females, with 53% and 47%, respectively, and the largest age group was 25 to 34 years.

Income Levels

On average, Australian consumers own 1. 8 BNPL accounts. Nevertheless, 51% of consumers have one account, 31% have two accounts, and 12% have three accounts. About 5% of Australians have four or more accounts. Notably, those with multiple BNPL accounts are more likely to be low-income earners (those earning less than $35,000 per annum).

Impact of BNPL on Australian Consumer Spending Habits

BNPL products have become increasingly popular among consumers in Australia over the last few years. A 2021 Reserve Bank of Australia report showed that there were between 3-4 million active BNPL users in the country as of June 2021, up from 30% of the prior year. The current major players in the BNPL market in Australia include Afterpay, Zip Pay, OpenPay, and many others, and most of the market share is controlled by these significant providers.

The BNPL platforms are also revolutionising how Australians pay for purchases and giving them control over credit. BNPL is Australia's most-used online payment method, behind credit/debit cards and PayPal.

More than half of the survey participants reported using BNPL services. The drivers for BNPL include making purchases without the need for credit checks and long application procedures, splitting the payment without any interest charged between 4-6 instalments, and budgeting.

BNPL is influencing Australian consumer spending patterns in several key ways:

- Increased purchase frequency: 15-30% of consumers use BNPL to make more frequent impulse purchases. The flexibility of the BNPL credit line also leads to more impulse and repeat purchases.

- Higher average order values (AOV): BNPL transactions are relatively small, averaging $150, while credit and debit card purchases in Australia average $86. Since it removes affordability hurdles, BNPL enables consumers to spend more per purchase.

- Specific vertical growth: Specific industries such as fashion, beauty products, and electronics are particularly benefiting from BNPL. For instance, fashion accounts for 20 per cent of the total dollars spent through Afterpay internationally. These sectors target key BNPL demographics.

- eCommerce acceleration: Businesses that provide BNPL at the point of purchase have observed twice the typical order value for eCommerce merchants. With BNPL enabling more significant and more frequent online purchases, it drives the growth of eCommerce in Australia.

However, there are also increasing concerns about the ability to increase the level of credit consumer debt and the risks that arise if BNPL consumers borrow beyond their capacity to repay. Further reforms in the BNPL sector may be implemented in the future as it undergoes further development. Sustaining responsible growth while ensuring consumer purchase protection will remain a challenge in this area.

BNPL Providers: A Comparison of Major Players in the Australian Market

The BNPL market has been rapidly growing in Australia in recent years. Survey data from the Reserve Bank of Australia has revealed that Australians made $16B worth of BNPL purchases in 2021-2022.

The three biggest BNPL players in Australia are Afterpay, Zip, and the Humm group.

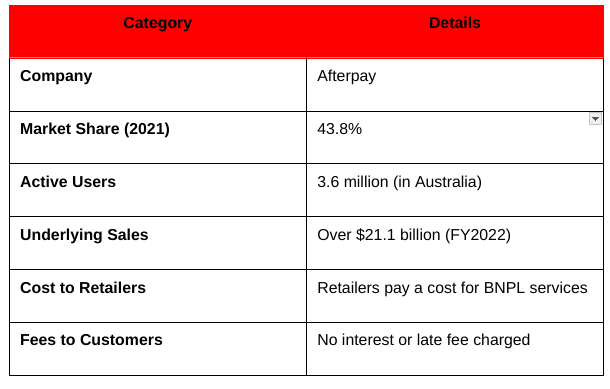

Afterpay Market Share

Afterpay has the highest market share, and it is expected that it control 43.8% of the market as of the fiscal year ended in 2021. According to company figures, it has 3.6 million active users in Australia and has processed over $21.1 billion of underlying sales through its networks in FY2022. Afterpay involves retailers paying a cost for BNPL services while no interest or late fee is charged to the customers.

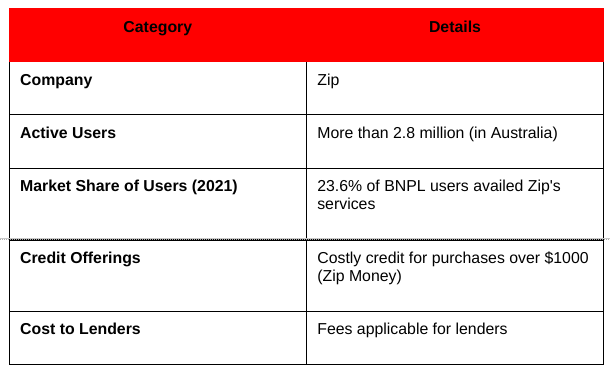

ZIP Market Share

Zip is another key participant in the market, with more than 2.8 million active users in Australia. A 2021 survey of BNPL users revealed that about 23.6% of them had availed of Zip’s services. Zip also provides costly credit for purchases of more than $1000 through Zip Money and gives lenders a cost.

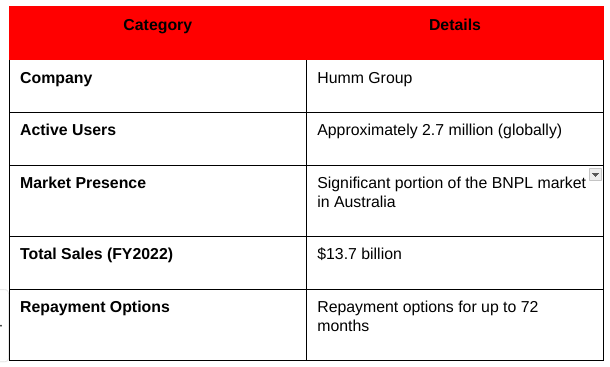

Humm Group Market Share

Humm Group, providing its services through Bundll, humm90, and Oxipay has approximately 2.7 million active users globally, with a significant portion of the BNLP market in Australia. These consumers engaged in these services, resulting in $13.7 billion in total sales for FY2022. They offer repayment options for up to 72 months.

Regulatory Landscape and Future of BNPL in Australia

The BNPL industry has expanded quickly in Australia in the last several years. It has been estimated that payment solutions provided through BNPL now capture 37% of all internet purchases in Australia. Some of the major BNPL players in Australia are Afterpay, Zip, and Humm, which operate with many active users. Nonetheless, the BNPL services have also received enhanced regulatory attentiveness. To this date, the BNPL providers in Australia do not need to conduct a credit check or determine the borrower’s repayment capacity. Late fees that BNPL platforms can charge customers are also not regulated with a maximum amount that can be charged.

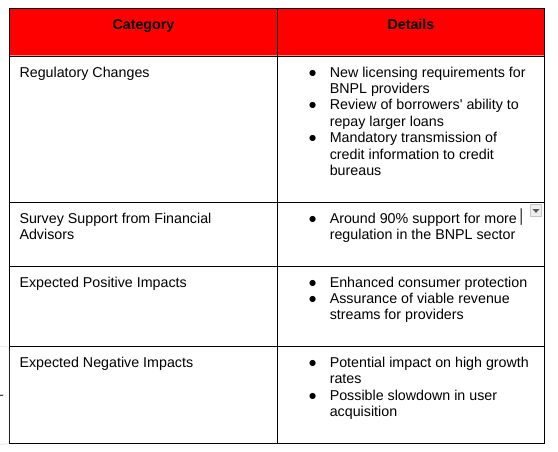

At the end of 2021, the Australian government amended and restated regulations for BNPL under the National Consumer Credit Protection Act 2009. The reforms bring new rules for BNPL providers to obtain a license and review the borrowers’ ability to repay larger loans. Providers will also have to transmit credit information about the customers to credit bureaus. A 2023 survey of financial advisors found that around 90% of them want more regulation for the BNPL sector. These changes might affect the high growth rates and fast user acquisition that BNPL companies have experienced so far. However, opponents state that it will also enhance consumer protection and guarantee BNPL’s viable revenue streams for providers. Further changes to the regulation of BNPL in Australia can still be expected. BNPL debts have been a concern to the Reserve Bank due to their effects on consumer credit ratings and increasing household debt. A more stringent regulation of the rapidly growing BNPL sector is likely essential to avoiding the financial crisis. The next size of the BNPL market will most probably depend on new regulatory measures that will manage to support innovation and competition from the BNPL platform and prevent the abuse of the recently adopted payment solutions. Finding the middle ground will be important.

BNPL and Financial Health: Risks and Benefits for Australian Consumers

Buy Now, Pay Later (BNPL) solutions are quite popular in Australia. They allow consumers to purchase goods without paying the full price at once. However, like financial institutions, BNPL has advantages and disadvantages.

Potential Risks

- Debt Accumulation: One potential threat is consumers getting into a situation where they are unable to meet the repayment cost while making multiple purchases without thinking of their ability to repay. This is prevalent among persons who are already struggling financially.

- Impact on Credit Scores: Though approval is frequently given without checking credit history, non-payment affects credit scores. Late penalties and delinquencies can be reported to the credit bureaus thus affecting chances of getting a loan.

- Financial Stress: Some users experience financial concerns due to additional charges incurred in the case of delayed payment. This hardship can snowball if individuals open several accounts to manage debts.

Benefits

- Budgeting Assistance: Extending expenses over weeks or months can help consumers manage their budget and ensure proper funding for consumption on the acquisition of large and significant products.

- Interest-Free Payments: Another very attractive factor is the no-interest payment option. In this respect, the fact that payments are made on time ensures the avoidance of high credit card interest rates.

- Consumer Convenience: These services facilitate fast and easy purchases, whether through the Internet or physical retail department stores. Many retailers have already implemented this, making this convenience possible.

BNPL Usage Trends During Major Shopping Events

Buy Now, Pay Later services have been observed to rise during prominent purchasing occasions such as Black Friday, Cyber Monday, and Boxing Day sales in Australia. These occurrences affect consumer expenditure, and BNPL services are a perfect solution to their needs.

Black Friday and Cyber Monday

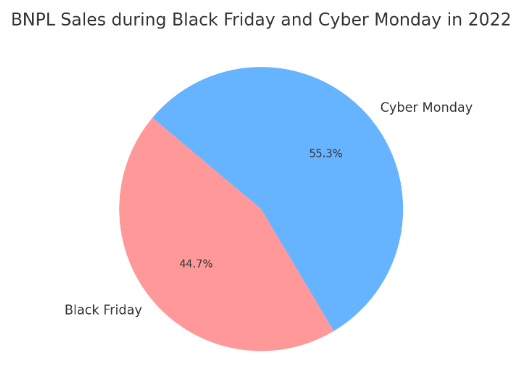

In 2022, BNPL sales during Black Friday reached $9.12 billion, a 2.3% increase over the previous year. Cyber Monday sales reached $11.3 billion, marking 5.8% total growth year over year. The jump in sales is mostly from toys, electronics, and computer purchases.

Overall Holiday Season

The use of BNPL services is becoming unstoppable whether it's a holiday or just a normal day, and Black Friday and Cyber Monday are the living proof of that. The fact that this service provides people with better BNPL options in purchasing the things they want without needing to pay upfront. The increase in spending is something that cannot be ignored.

The Impact of BNPL on Traditional Credit Products

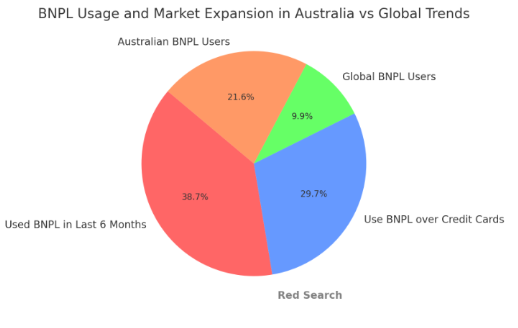

The buy now, pay later market has expanded significantly in Australia; 43% said they used BNPL in the last 6 months. A current finder survey reveals that BNPL is used by 33% of consumers than credit cards, thinking they'll be more in debt using credit cards. It is evident that emerging BNPL solutions, including Afterpay and Zip, are disrupting traditional credit solutions.

A survey in 2021 shows that Australian BNPL users are 24% , even higher than the 11% users globally. This trend has continued until now, as many are shifting to BNPL services rather than traditional credit card companies. Though 2022 RBA data said that there are still over $13 million of credit card users in the country, this number is slowly declining due to the increase in BNPL service users. From the consumer’s perspective, BNPL is an interest-free instalment payment solution with reasonable payment terms. It also assists the consumers in spreading the costs with no need for credit checks or even considering credit scores. However, financial experts argue that BNPL popularises debt among young people. Other issues include financial overextension, charges, and the fact that regulation has not been able to keep up with BNPL's growth. With the growth of digital payments, BNPL is positioning itself as the preferred payment method among online consumers over traditional credit products such as credit cards. These numbers mean that BNPL is not going anywhere anytime soon, as its revenues increased by over 90% in 2021.

Consumer Awareness and Attitudes Towards BNPL

According to a 2022 survey conducted by the Australian government, 81.1% of consumers have heard about BNPLs such as Afterpay among younger demographics. The majority of BNPL consumers are below 40 years old, with the main reasons for using the product being convenience, better control over spending, and avoiding credit card debt. BNPL users face repayment issues as per ASIC , especially the young population. While RBA states that the BNPL sector may lead to stability issues for households through escalating debt levels, users mostly use BNPL services without considering how they will pay afterwards. The convenience that BNPL services bring to people makes others spend more without thinking.

BNPL and Online Retail: The Symbiotic Relationship

With the BNPL services, Australians have benefited from the promotion of the online retail industry. It is estimated that 7 million Australians used BNPL in 2022, with $16 billion in BNPL transactions . Big players in the BNPL sector such as Afterpay, handled more than $21 billion in sales in 2022 Consumers understand that BNPL does not incur any interest, which is why BNPL users prefer this method of credit more than they like credit cards. This is because costs are paid in instalments, thus increasing customers' BNPL purchasing power. However, critics have claimed that the lack of strict monitoring has led to the expansion of the use of BNPL. For instance, credit limits and less stringent credit checks mean that BNPL leads to reckless consumption and, therefore, unmanageable debts to low-income earners. Some financial institutions have expressed concerns and provided negative feedback, though it is currently not rated highly among consumers. With the ever-growing online retail market, one can only notice how the relationship between BNPL and e-commerce sites is becoming more intertwined.

Future Predictions for BNPL in Australia

Future market saturation and rise in regulatory measures may act as headwinds to growth. The Australian government assesses the BNPL legislation to safeguard consumers, and the Reserve Bank says BNPL may lead to risky household credit. Reduced approval by BNPL providers may lock out some users.

Even the mainstream credit card issuers are providing similar 0% financing to keep up with the competition. As mentioned earlier, BNPL is fashionable now with market share wars with banks and regulatory changes implying that growth may slow down. Finally, there is still growth potential for BNPL in Australia but it is not clear that growth will continue at such a rapid rate.

For more on Australian statistics, see our other articles:

- Australian Mobile Phone Statistics

- Australian Internet Statistics

- Australian Google Trend Statistics

- Australian eCommerce Statistics

- Australian Christmas Online Shopping Statistics

- Australian Local SEO Statistics