The Rise of Buy Now Pay Later (BNPL) in Modern Shopping

The rapid growth of online shopping driven by shifting needs from the pandemic to today’s new normal has propelled BNPL in Australia. From consumers turning to alternative financing options to Gen Z looking for convenient and accessible payment terms, BNPL offers new features that mainly work well with younger consumers.

BNPL allows consumers to split large purchases into smaller instalments at zero interest. As a result, this payment option has transitioned from a niche digital payment to a mainstream checkout option for savvy consumers.

What is BNPL and How Does It Work?

Buy now, pay later (BNPL) is a short-term financing option that allows consumers to pay instalments over time. It’s a point-of-sale (POS) short-term loan that usually doesn’t charge interest.

Consumers can traditionally take advantage of BNPL services at the check-out counter, via online retailers in eCommerce shops, or through apps provided by third-party BNPL services.

Source: Investopedia Compared to credit cards, applying for a BNPL payment takes a short time, sometimes with less protection than credit card facilities. Nonetheless, consumer approval remains high, as the Consumer Financial Protection Bureau (CFPB), 69% of applicants between ages 18 and 24 qualify for BNPL loans.

BNPL loans are an excellent option for young consumers and Gen Zers who don’t have the required credit score or have insufficient credit history to qualify for a traditional credit card.

A Snapshot of BNPL Growth

In 2023, Australia’s buy now pay later market was valued at US$ 7.14 billion and is forecasted to reach US$54.87 billion by 2030, achieving a CAGR of 28.5% from 2024 to 2030.

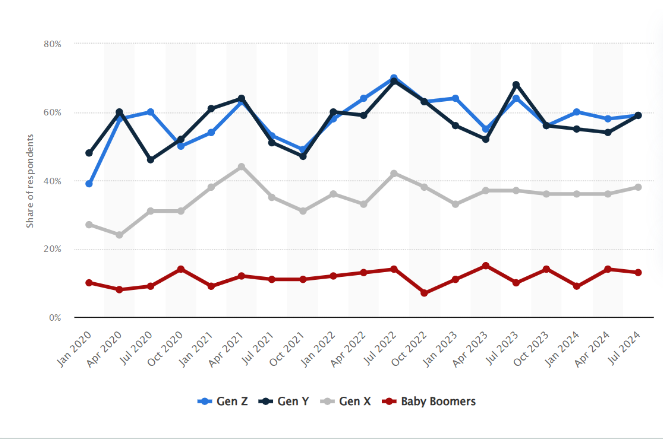

Younger consumers primarily drive that market value, as most Gen Z and Gen Y shoppers (59%) consider using BNPL as their eCommerce payment option compared to other options.

Source: Statista

Why Gen Z Prefers BNPL Over Traditional Payment Methods

Affordability and Accessibility

Unlike credit cards and traditional loans, BNPL programs offer short-term loans with zero interest and no additional charges. That means budget-conscious Gen Z consumers already know how much they’ll pay each month in interest-free instalments, allowing for easier and more flexible budgeting.

Instant Gratification Culture

BNPL attracts a generation that highly values flexibility and instant gratification thanks to its minimal barriers to entry. Put social media into the frame, and you’ll understand how digital trends encourage digital natives to make quick purchases without requiring full payment.

Distrust of Traditional Credit Cards

Younger consumers, particularly Gen Zers, are often cautious about accruing interest due to their current buying power and are very wary of hidden fees. Unlike traditional credit cards, these BNPL services offer interest-free flexible instalments, making them popular with Gen Z.

Tech-Savvy Integration

The rise of BNPL services reflects a noticeable shift towards tech-savvy lifestyles and more transparent & straightforward terms. You can even find BNPL services integrated into apps and eCommerce stores, aligning with digital natives who prefer modern alternatives to traditional credit and debit.

Explain how BNPL seamlessly integrates with online shopping platforms and mobile apps.

How BNPL Aligns With Gen Z Values

Flexibility and Freedom

As discussed earlier, BNPL is a payment solution that is customisable to an individual’s preferences. Its flexibility, transparent billing, and interest-free payments allow buyers to budget their expenses and pay without incurring steep interest fees.

Furthermore, 70% of Gen Zs use BNPL for purchases less than $100. This highlights BNPL’s ease of use and availability as a product integrated within eCommerce stores, digital wallers, and an alternative to credit cards.

The University of New South Wales reported that more than 1 in 3 Australians regularly use a smartphone integrated with a digital wallet to make in-person payments. GlobalData reports that over 15.3 million payment cards were linked to digital wallets in 2022, reaching up to AU$209 billion in fees by 2024.

It’s safe to say that very few Gen Zers still rely entirely on physical cards.

Social Media Influence

Shopping habits don’t fall too far from lifestyle influence. That said, Gen Zers have purchasing habits that are widely influenced by what they digest on social media.

About 1 in 3 (31%) of Gen Zers have bought an item after seeing it in a social media advert. Almost the same percentage of Gen Z consumers (33%) have purchased an item after seeing someone they know post about it on social media, with 39% of females influenced this way.

Source: Opinium

The Impact of BNPL on E-Commerce Growth

Boosting Conversion Rates

BNPL is highly regarded for its transparency, encouraging more conversions, and eliminating sticker shock when the checkout price is too overwhelming. As a result, BNPL boosts conversion rates up to 30% as customers can make bigger purchases, knowing they don’t need to pay for everything upfront.

Expanding Customer Demographics

The rise of BNPL comes with shifting financial behaviours as more Australians rely on digital payments and tech-forward shopping experiences provided by mobile apps and eCommerce stores.

Younger Australians, especially those under 35, rely on BNPL as a viable alternative to credit cards and short-term loans. BNPL becomes a boon for retailers when wallets tighten, as Gen Z and younger audiences with minimal savings can purchase goods they can’t afford.

Increasing Average Order Value (AOV)

Most BNPL purchases are relatively small, averaging at only $150. However, credit and debit card purchases average only $86. Since BNPL removes affordability hurdles, savvy consumers are encouraged to spend more per purchase.

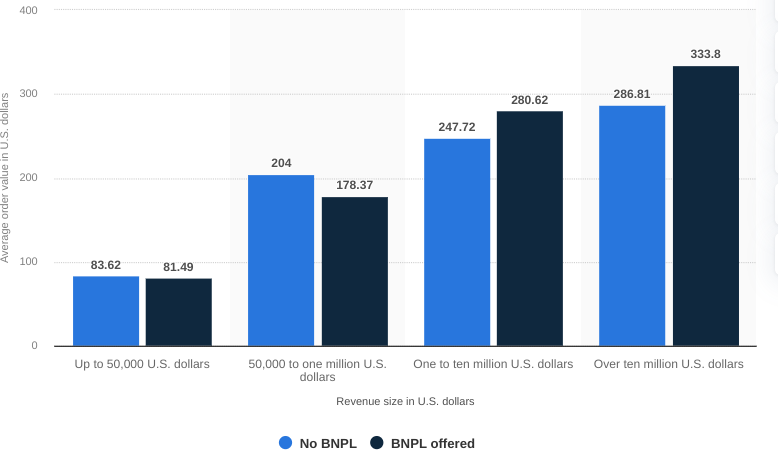

In 2023, a global study on eCommerce revenue showed that stores offering BNPL options with annual revenue between 1-10 million US dollars had an average order value of $280.62. The trend stays true for stores with over $10 million in annual revenue, but smaller businesses generating up to $50,000 and $1 million show a slight correlation.

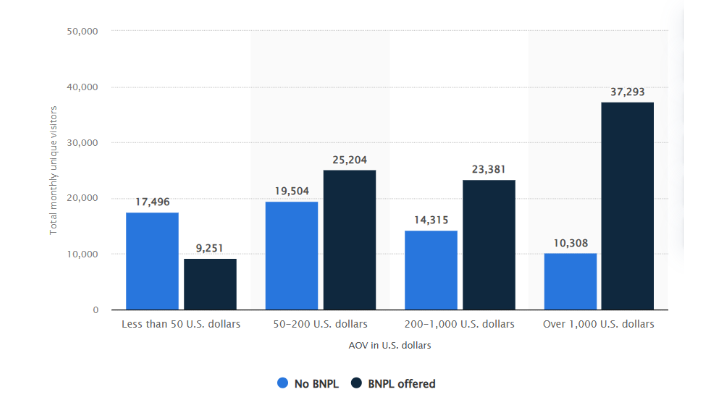

Source: Statista Moreover, online stores offering BNPL options report higher traffic. Another report shows that shops with over $10 million in annual revenue offering BNPL have about 27,000 more monthly unique visitors than those without BNPL.

Source: Statista

Challenges of BNPL and How Businesses Can Address Them

Potential Risks for Consumers

Unlike traditional credit cards and loans, the National Credit Code does not cover BNPL lenders, meaning they don’t have the same legal obligations as banks and lenders.

That means BNPL lenders are not obliged to:

- Verify that you can afford repayments

- Offer hardship clauses when you can’t meet repayments

- Be a member of the Australian Financial Complaints Authority (ACFA)

However, there are BNPL lenders who are members of the ACFA and provide some protections to its consumers, including:

- Make sure the BNPL product and term are suitable for you

- Have a formal complaints process that’s easily accessible from the app/website

- Offer financial hardship for consumers experiencing financial difficulty

- Comply with ACC’s and the Australian Securities & Investments Commission’s Debt Collection Guidelines.

Aside from customer service and credit protection, BNPL also poses potential risks associated with overspending and debt accumulation, especially to Gen Z consumers who are more likely to use BNPL products than non-Gen Z buyers (28% compared to 21% of non-Gen Z).

Younger audiences, particularly those with limited financial literacy, are susceptible to impulsive purchases and the urge to satisfy instant gratification. As a result, BNPL shopping sprees can lead to a cycle of debt that negatively impacts long-term financial health.

Consumers should approach BNPL purchases responsibly and cautiously, keeping themselves aware of their spending limits and budget while prioritising timely repayments.

On the other hand, businesses can promote responsible BNPL usage by clearly displaying their terms and conditions while placing visible reminders encouraging mindful spending throughout the buyer journey.

Frequently Asked Questions

Conclusion

BNPL services have revolutionised how Gen Z consumers shop and purchase. Offering flexible payment options that seamlessly integrate with digital shops and smartphones complements a tech-savvy generation.

As more businesses appreciate the potential of BNPL options to boost engagement and checkout values, they must adapt to the evolving needs of younger consumers, especially those empowered by influencers and effective digital marketing strategies.